Just as the global economy appeared to be stabilising after a series of shocks, the latest geopolitical conflict threatens to derail progress. While a temporary ceasefire provides short-term relief, the absence of a lasting resolution keeps markets on edge, with oil prices surging to levels not seen since the 2022 energy crisis.

The economic fallout will depend on how long the disruption lasts, the extent of infrastructure damage, how policymakers respond and which countries are most vulnerable energy importers.

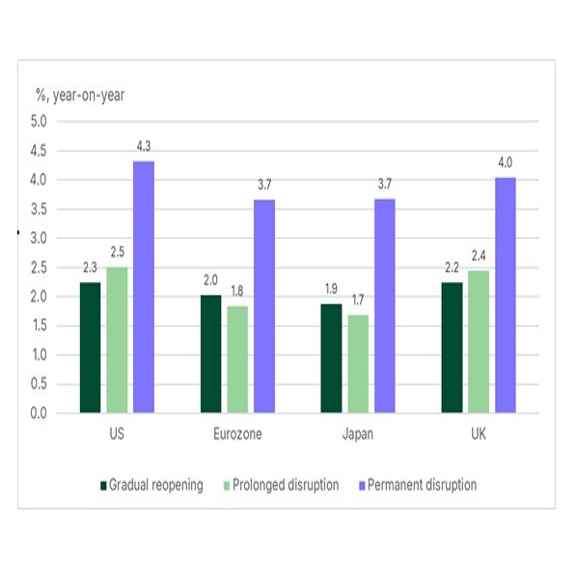

Three possible scenarios for the global economy

The severity of the economic impact hinges on how long the Strait of Hormuz remains blocked and whether the conflict escalates. We have modelled three scenarios, each with distinct implications for energy prices, inflation and growth.

1. Gradual reopening

If the Strait reopens by mid-2026 and shipping stabilises by year-end, oil prices may peak in Q2 2026 before falling to back to pre-war levels. This would trigger a brief inflation surge with minimal growth slowdowns. The US, as a net energy exporter, would face fewer disruptions, while Asia’s reliance on Middle Eastern oil would pose greater risks.

Central banks would likely tolerate temporary inflation, avoiding (sharp) rate hikes. Fiscal support would target vulnerable households, and some emerging markets (for example Indonesia) might accelerate renewable energy adoption to reduce future fossil fuel exposure.

2. Prolonged disruption

The ceasefire fails initially, with ongoing closure of the Strait and additional infrastructure damage. A more durable agreement is reached later in Q2, allowing gradual reopening of the Strait. We assume oil prices peak in Q2 and return to their pre-war levels in the second half of 2027. Inflation would rise more sharply, while growth would slow significantly. Japan could enter recession and Southeast Asia’s oil-importing nations (Philippines, Indonesia and Vietnam) would face severe strain.

Central banks likely respond with rate hikes to curb inflation, while governments could widen fiscal deficits to extend fuel subsidies. Some countries might (continue to) temporarily lift sanctions on Russian oil or increase coal use, delaying the energy transition.

3. Permanent disruption

If the Strait remains closed through 2026 and the conflict escalates into a broader regional war, oil prices could surge to on average USD 150 per barrel in Q4 2026, triggering a sharp and prolonged rise in inflation and a global recession. In this scenario, the global confidence shock outweighs any gains from being a net energy exporter and will likely result in social unrest in low-income countries.

Central banks would likely hike rates aggressively and governments would implement widespread fiscal stimulus, though debt constraints could limit effectiveness. Energy rationing might become necessary in some emerging markets.

Impact on advanced economies

The US, as a net energy exporter, will weather the storm better than most if the conflict stays relatively contained, though it will stay exposed to global energy price increases. Europe and especially Japan, however, would face both higher inflation and a significant growth slowdown. The European Central Bank, Bank of England and Bank of Japan would therefore need to balance inflation control with growth protection, avoiding over-tightening monetary policy.

Impact on emerging markets

The Gulf countries, produce around 30% of the world’s oil. As the epicentre of the conflict, the Middle East countries are suffering most acutely. Investment activities have largely stalled and the tourism sector has been significantly damaged. Unemployment could rise by 4%, disproportionately affecting migrant workers and reducing critical remittances. Asia, heavily reliant on Middle Eastern oil imports, faces fuel shortages and price spikes, particularly in nations with low reserves. Coal use could rise, slowing the energy transition. Governments may impose energy-saving measures and subsidies, straining budgets. Other oil exporters like Brazil, Mexico, Nigeria and Angola profit from higher prices, while importers like Chile, South Africa and Kenya risk inflation and currency depreciation. Low-income nations could face debt crises if disruptions persist.

Energy transition at a crossroads: threat or opportunity?

The current crisis has exposed the fragility of global energy systems, but it could also accelerate the shift to renewables. The outcome depends on policy choices. Higher oil prices could incentivise more drilling in Africa and Latin America, while coal demand could surge further in emerging Asia. Fossil fuel subsidies, if extended, would distort markets, making renewables less competitive and delaying the transition.

At the same time, the cost of solar and wind power has plummeted and energy storage demand is rising. If governments allow fossil fuel prices to reflect real shortages and provide targeted support for those most in need, renewable energy prices would become even more competitive. Some governments are already acting: Indonesia is replacing diesel plants with solar and battery storage, Europe is doubling down on renewables and energy efficiency and the US is investing in hydrogen and carbon capture.

The key question is whether governments will use this crisis to fast-track the energy transition or double down on fossil fuels, perpetuating geopolitical risks.