2025 has underscored both the urgency and complexity of addressing climate change. Global greenhouse gas emissions reached a new record of 60.63 billion tonnes of CO₂ equivalent. Average temperatures again surpassed historical records and prolonged heatwaves and severe flooding disrupted communities and supply chains worldwide. At the same time, regulatory expectations are rising. New climate disclosure requirements worldwide reinforce the need for transparency and accountability.

Listed companies, especially the highest emitters in our portfolios, face growing pressure. They are expected not only to set ambitious targets, but also to show credible and actionable pathways toward decarbonisation and resilience.

Change in our engagement approach

Our climate engagement prioritises the companies with the highest greenhouse gas emissions across our Impact Equities and Bond portfolios, and who run the highest climate risks. Annually, we select the top 5 highest emitters per fund. While our minimum standards aim to exclude the most harmful climate activities, we still have exposure to energy-intensive sectors such as utilities, industrials and chemicals.

Several companies consistently rank among the top emitters, and we engage with them regularly, building on previous discussions. With others, we only began climate-focused dialogue in 2025. Our discussions are tailored to each company’s climate strategy. They typically address greenhouse gas (GHG) emissions disclosure, reduction targets, implementation strategies, energy management and physical climate risk. Where possible, we monitor progress, offer targeted feedback and encourage continuous improvement in both strategy and reporting.

After several years of engagement, we observe notable progress. Many portfolio companies have reduced GHG emissions, mainly through energy efficiency and increased renewable energy use. This has lowered emissions across our Impact Equity and Bond portfolios. For example, chemicals manufacturer Evonik is transforming its operations through process efficiency, site upgrades and phasing out carbon-intensive assets such as coal-fired power. Lion, a Japanese consumer goods producer, is expanding renewable electricity procurement and using internal carbon pricing to support decarbonisation.

Scaling up climate finance with smarter climate risk insights

Initially, our engagement focused on emissions reporting and target-setting. Now, most companies report across all three scopes and have set ambitious targets. This shifts our discussions to new challenges. We now focus more on meeting targets, improving Scope 3 reporting and addressing physical climate risks.

Key themes from 2025 engagements

- Scope 3: moving from measurement to action

Companies are making progress on operational emissions. Scope 3, however, remains one of the most complex and critical frontiers. In 2025, our dialogues showed increasing transparency around these challenges, alongside early signs of more actionable strategies.

For example, Brazilian water and sewage treatment company SABESP has taken steps to improve its emissions inventory and data quality. It now includes emissions from untreated sewage in its Scope 3 inventory. This shows a willingness to improve the quality and transparency of its reporting. This is especially positive because sectors such as utilities, emissions are structurally hard to measure. Similarly, Italy’s leading electricity transmission system operator Terna highlighted the complexity of Scope 3 emissions linked to grid losses and transformer use-phase emissions. This shows how sector-specific factors can strongly shape emissions profiles.

At the same time, companies such as Owens Corning and SNCF are taking clear steps to reduce scope 3 emissions. Owens Corning, a building and infrastructure products supplier, is strengthening supplier engagement and circular product design. French railway company SNCF is pushing its suppliers to set their own science-based targets. These approaches show a shift from only measuring emissions to actively engaging the value chain. At the same time, implementation is still uneven and often limited by data availability and how ready suppliers are to act.

- Resilience and physical climate risk

The physical impacts of climate change are becoming more important in corporate strategy. This is driven by stricter reporting rules and the tangible effects of extreme weather events on operations, supply chains and energy availability. As a result, companies are more aware of risks such as storms, flooding and heat stress. They are starting to turn this awareness into more concrete plans for resilience and adaptation. These plans still differ in depth and implementation. But this shift shows growing recognition of the need to protect assets and operations, strengthen long-term continuity and mitigate the financial risks of increasing climate-related physical risks.

British energy transmission and distribution company National Grid, for example, sees storms as a key operational risk. It is investing in infrastructure reinforcement and AI-driven prediction tools to better anticipate and respond to extreme weather. SABESP is upgrading its water and sewage systems to become more resilient to climate variability. Terna is incorporating climate risk considerations into its grid management and service continuity planning.

In other sectors, physical and transition risks are becoming more connected. Ingredion, a global ingredients solutions company, recognises that its exposure to agricultural supply chains vulnerable to drought and extreme weather makes climate risk central to both its operational and sourcing strategies.

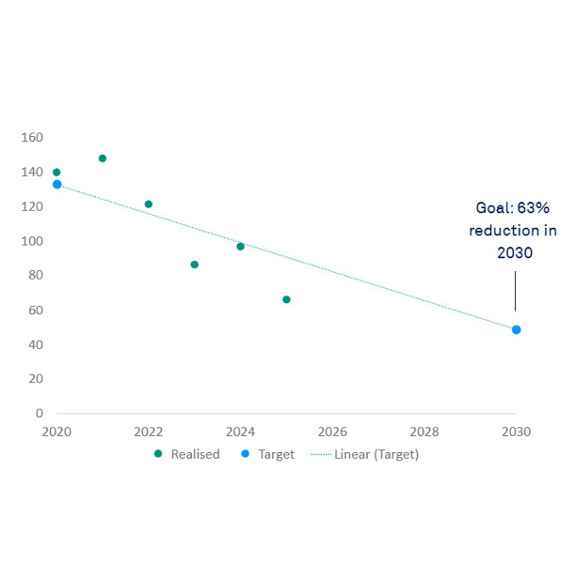

Scope 1+2 emissions trajectory

The reduction of scope 1+2 GHG emissions of the Impact Equities and Bond portfolios by 2030 is part of the SBTi-approved reduction target of Triodos Bank. These are absolute emissions by our investees. We aim to meet this target through engagement efforts and portfolio allocation. The chart shows that our investees have achieved meaningful reductions so far, on track with our target.

What's next?

The 2025 engagement cycle shows that, although challenges remain, a significant number of companies is taking steps to develop and implement a climate strategy. The companies included in our engagement programme are moving beyond high-level commitments. They are working on more detailed, actionable strategies that address both emissions reduction and climate resilience.

At the same time, the complexity of the transition, particularly around scope 3 emissions and physical climate risks, calls for ongoing dialogue, technical innovation and commitment.

By continuing to refine our approach, we keep engagement as a key tool for holding companies accountable for climate-related issues. Despite global turbulence and setbacks in climate commitments, sustained dialogue allows us to promote more transparency and encourage more robust, forward-looking climate strategies. Engagement on climate change-related topics remains key in supporting long-term sustainable corporate resilience.