Energy markets have rarely been as turbulent as they are today. From the vital shipping lanes of the Strait of Hormuz to the conflict zones in Ukraine, geopolitical tensions are shaking global supply chains, driving up price instability and inflation, and exposing the fragility of how our world is powered.

Two priorities are clear: eliminating reliance on gas-fired 'peaker' plants used during demand spikes, and ensuring grid stability in systems that are increasingly dominated by variable renewable energy.

Renewables are now central to both climate strategy and energy security. Scaling them effectively will require coordinated investment and deployment. Not only in generation, but also in grid infrastructure and, critically, in energy storage.

Reducing fossil dominance in grid balancing

For decades, utilities across the US, Europe, Japan and Australia have relied on natural gas peaker plants and other gas-fired plants to meet spikes in demand. These plants operate infrequently but are extremely carbon-intensive.

Battery energy storage systems (BESS) are now emerging as a viable alternative. By storing excess renewable energy during periods of low demand and discharging it during peak hours, batteries can replicate, and often outperform, peaker plants.

Modern battery systems offer even more. They provide essential grid services such as frequency regulation and voltage support, functions historically delivered by fossil fuel-based generation. Batteries are evolving into multi-functional infrastructure, capable of supporting peak demand, balancing supply and maintaining reliability.

The rapid evolution of these technologies has fueled strong growth in battery deployment in recent years. However, this progress is now colliding with geopolitical tensions, expectation of rising inflation and interest rates, as well as shifting industrial policies in both China and the US. The pressing question is whether the momentum will continue or fragment.

What’s driving the battery boom

On the demand side, renewable energy is benefitting from rising electricity needs, including for AI-driven data centres. These centres are straining fossil-heavy grids and pushing tech companies to seek cleaner energy sources. Additionally, growing populations are driving up final energy consumption, which in turn supports increasing renewable energy penetration, as consumers look for affordable and stable energy sources.

On the supply side, as more countries embark on a path to net-zero, governments are becoming facilitators of renewable energy adoption by introducing various incentives. At the same time, disruptions to fossil fuel supplies, particularly those stemming from tensions in the Middle East, are prompting governments to rethink their energy mix, placing greater emphasis on self-reliance through renewables.

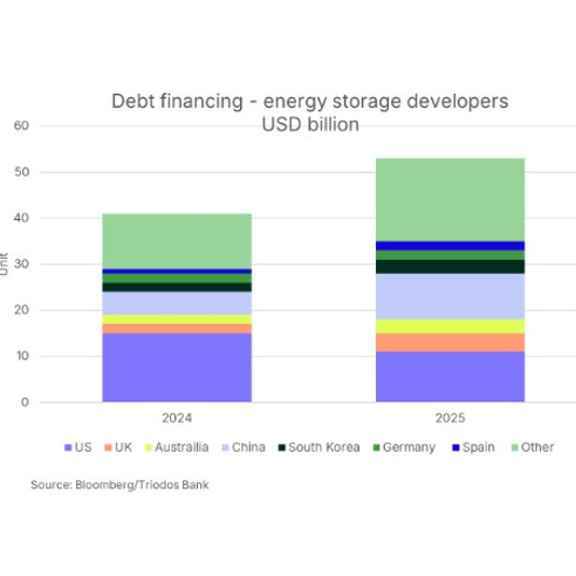

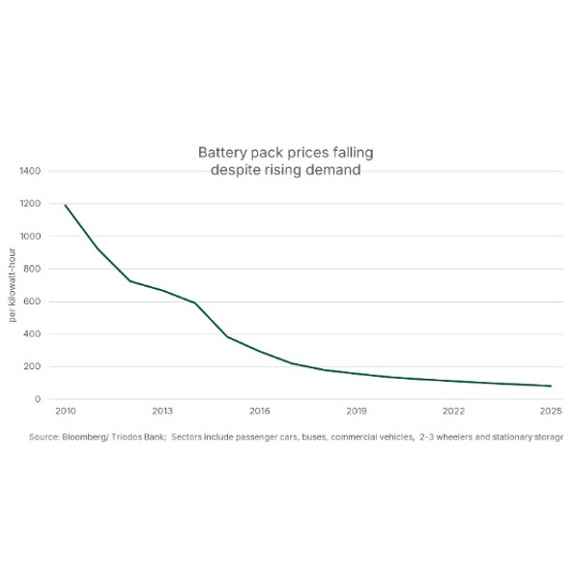

According to Bloomberg, global stationary energy capacity grew by 65% between 2024 and 2025 and is expected to grow by 58% in 2026. China, the US, Australia and the UK lead deployment, with Saudi Arabia emerging quickly. Falling battery prices, down 9% in both 2024 and 2025 respectively, are supporting this growth.

At the same time, battery supply chains are under strain due to geopolitical tensions and supply and demand imbalances, particularly in China. Overcapacity is pushing Chinese producers to expand overseas. However, this has become more challenging with the US tariffs and a growing protectionist trend focused on for energy self-security. As a result, China’s access to other markets is increasingly being restricted.

When the grid can’t keep up

While cost and capacity dominate much of the discussion, they are not the only challenges facing electricity grids. Most existing grids were designed for centralised, fossil fuel-based generation, not for decentralised, variable renewables. Integrating large shares of wind and solar creates new stability challenges. In this context, the role of batteries is evolving further. When paired with grid-forming inverters, battery systems can actively stabilise the grid.

Unlike conventional inverters, which simply follow the grid’s frequency, grid-forming technologies help create and regulate that frequency. They replicate the inertia and voltage support once provided by coal and gas power plants. The global market for grid-forming inverters is projected to grow from USD 850 million in 2025 to USD 1.73 billion by 2034.

Outlook for future renewable grid stability

Our 2026 economic outlooks consider different scenarios. Our current forecasts are based on the Strait of Hormuz gradually reopening and regional tensions easing toward the end of the year. In this scenario, global battery deployment continues to grow, although shifts in industrial policy may reallocate market leadership away from the US and China to a broader range of regions. Our alternative scenarios adopt a more cautious view in terms of the investment environment for battery storage, particularly in the Middle East. This region remains a growing market for battery storage production.

Ultimately, the battery storage revolution is not simply about replacing one technology with another. It is a response to an increasingly volatile energy landscape, where supply disruptions and geopolitical tensions continue to expose the vulnerability of fossil fuel-dependent systems. For countries historically dependent on imported fossil fuels and ageing thermal infrastructure, the combination of renewable generation and advanced storage offers a pathway to greater economic resilience and long-term industrial competitiveness.