When the recent energy shock hit the world, emerging markets were in relatively strong economic shape. The prolonged closure of the Strait of Hormuz undoubtedly added to inflationary pressures, but the impact on GDP growth has been relatively contained, except in Middle Eastern countries, where the damage has been significant.

When the energy shock hit, governments acted swiftly with subsidies, energy-saving measures, and renewable investments, while alternative oil routes and increasing exports of US strategic reserves stabilised supply. Lower oil demand from China also eased supply pressure. The global AI boom, led by the US and China, also cushioned the blow by boosting demand for semiconductors and emerging markets commodities like copper.

However, risks remain. The agreement between the US and Iran is fragile, trade tensions persist and food prices will still face upward pressure from the lagged effects of the disruption in the Strait of Hormuz. There is a silver lining though. The crisis has accelerated the shift to renewables, with solar, storage, and EVs gaining traction across Asia, Africa, and Latin America, reinforced by China’s capacity to satisfy the increasing global demand in clean energy.

Revised scenarios

We have updated our scenarios, published in April 2026. Back then, our most optimistic scenario expected an agreement to have been reached sooner. Since 28 February, Brent prices have averaged USD 106 per barrel, having peaked in April, for now, and moved between USD 70-80 per barrel since the recent announcement of a peace agreement in June.

Our adjusted global scenarios are built around different expectations for oil price paths:

- Reference scenario: Oil prices peak in Q2 and return to pre-conflict levels in the second half of 2027. This scenario is based on the prospect that the agreement recently reached to end the war on Iran will be sustained. So far, the agreement envisages a two-step approach, with a 60-day phase to determine the future of Iran’s nuclear programme.

- Oil prices peak in Q3: This intermediate scenario assumes that oil prices peak in Q3 and only ease towards pre-conflict levels in 2028. We think the sensitivity of the discussion around Iran’s uranium enrichment under this scenario could drag on into late Q3, with tensions lasting until then. Under this scenario, GDP growth of the two largest emerging economies - China and India - would decline moderately in 2026 and 2027. Both countries would probably rely more on alternative energy sources, including coal and new fuel blends, to support economic activity.

- Permanent disruption: If military action resumes and continues through the year, oil prices could peak in Q4. Further damage to oil infrastructure would likely push any return to pre-conflict price levels beyond our forecast horizon. Both China and India would face a sharp slowdown in GDP growth in 2027, reflecting the prolonged conflict. China would be hit harder than India, given its greater exposure to the global slowdown as a result of its strong trade linkages.

The near-term outlook

Based on the reference scenario, with corresponding mitigating actions to reduce the impact and the AI investment cycle continuing through the rest of 2026 increasing global demand for commodities and inputs from a wide range of countries, we expect emerging markets GDP growth to slow modestly to 3.7% in 2026, from 4.4% in 2025. Divergence across countries is sustained. The Middle East, in particular, borders on contraction.

Meanwhile, inflation is likely to become more material in the second half of the year. High inflation is driven by firming food price pressures and high transport costs, while services inflation signals are mixed due to weakening demand. We expect the average inflation rate to reach 5.4% in 2026, which is 1.2 percentage points above pre-conflict forecast levels. Core inflation is forecast to peak close to 3.7% year-over-year in Q4, about 0.5 percentage points above central bank targets and pre-conflict levels.

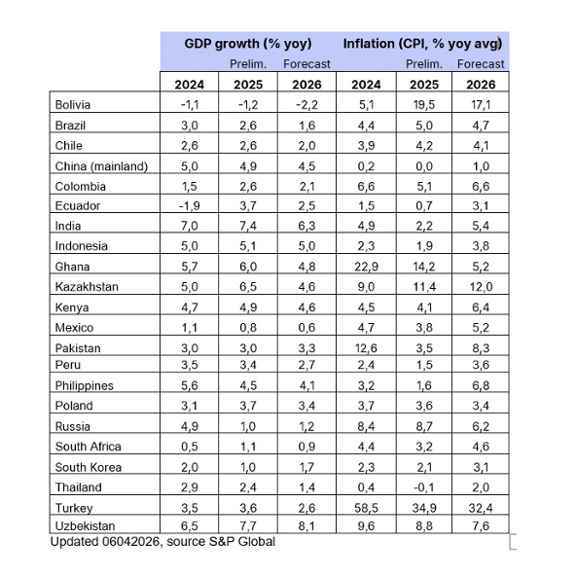

Forecasts selected countries

Advanced Economies: Energy security in an AI economy

Energy security and fair AI

Emerging markets have remained resilient amid global turbulence, supported by stronger fundamentals, credible central banks, flexible exchange rates and, in many cases, disciplined debt management. However, the effects of the Middle East conflict are unlikely to fade quickly, underscoring the need to consider how future crises can be prevented.

The lessons from the Middle East conflict are clear: energy is no longer just a commodity; energy security is now a cornerstone of society. Consequently, building renewable energy capacity is crucial. Beyond energy, it is time to prepare for fair AI adoption. AI adoption offers a path to leapfrog outdated growth models keeping in mind sustainability and inequality concerns. For investors, the future lies in backing the energy transition and inclusive tech to prevent future crises and drive sustainable progress.

Read the full mid-year Emerging Markets Outlook here.