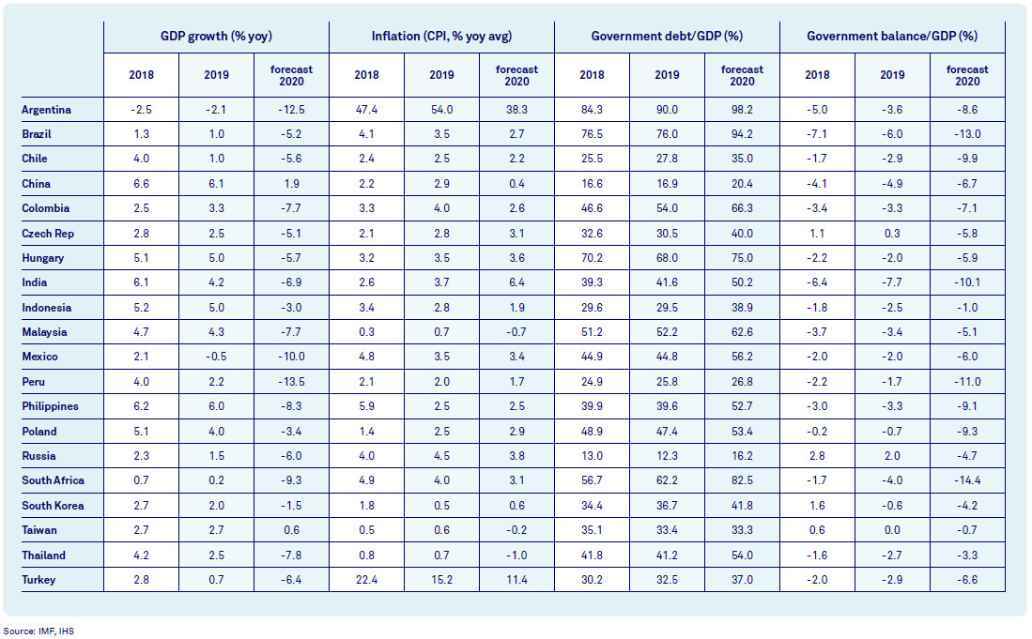

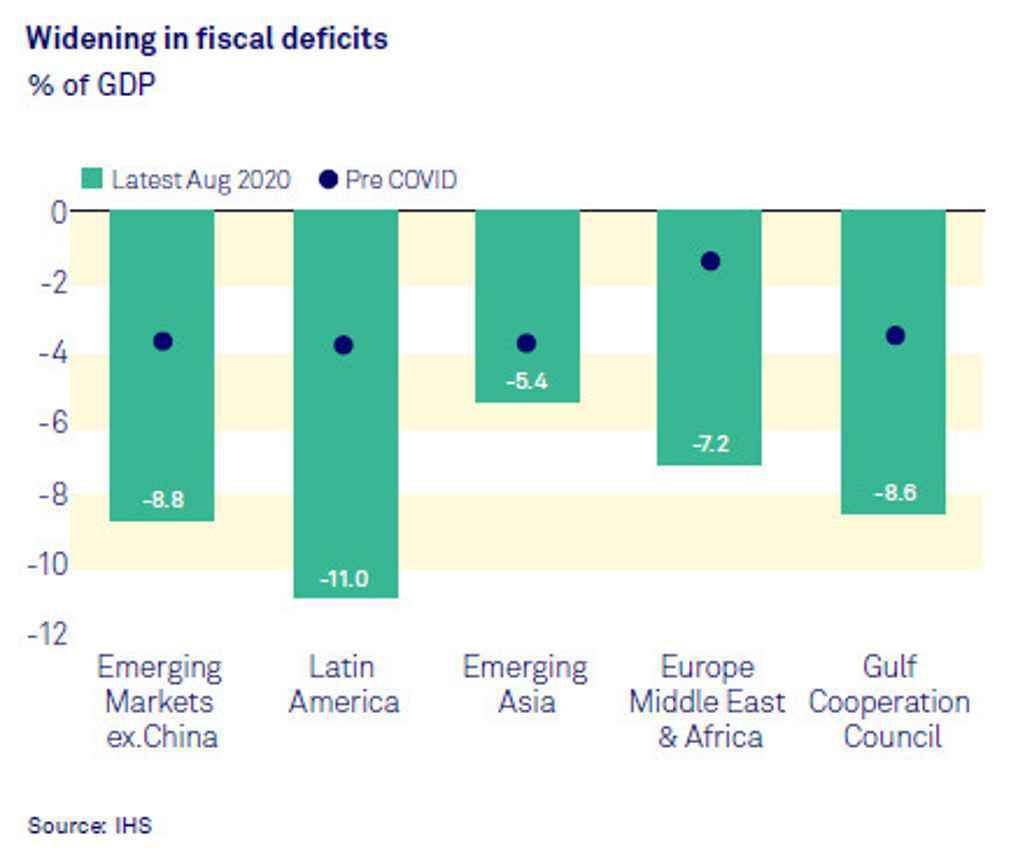

The pandemic has caused that almost all emerging and developing economies are seeing a uniform deterioration of budget balances and rising debt-to-GDP ratios. Although there are good reasons for this, there is a price to pay. Investors value fiscal discipline. Weaker fiscal positions make emerging markets more vulnerable to debt overhangs and spikes in risk premia, increasing their borrowing costs.

The fiscal costs of COVID-19

Read the full Emerging Markets Outlook.

There is a silver lining though. As countries enter a new stage of the recovery, governments are now playing a more predominant role, which could mean more room for impact investment directed at increasing economic resilience and improving well-being. Triodos IM, with its experience, will continue steering support in this direction.

Fiscal support and a V-shaped recovery

For fiscal spending to be effective it needs to translate to stronger and inclusive GDP growth. Governments and central banks have chosen different paths in providing stimulus, either through financials, nonfinancial firms or households, and if there was enough room, by providing stimulus to all sectors. The type of stimulus, its timing and size are setting the pace of the recovery. Going forward, the temporary nature of the stimulus will be critical in avoiding distortions, including crowding out of the private sector and moral hazard for the firms and households receiving government support.

For now, synchronised fiscal support has done quite a lot, but the V-shaped recovery is not for all countries. The most recent data suggest that the global recession has bottomed out in the second quarter. Investor sentiment has been improving in the first place towards advanced economies, and now also across emerging countries, particularly China, South Korea and Taiwan. However. those countries that entered the crisis in a weaker economic condition are still facing many risks, given that extraordinary financing and debt relief measures will not be enough to fill the large financing gaps that were already there prior to the pandemic.

Fiscal spending and reshaping long-term growth for better

International investors and rating agencies are sensitive to emerging market fiscal fundamentals and are less tolerant to higher debt levels. This has consequences on governments’ debt risk premia and investment returns over the longer-term. Additionally, local currencies are highly sensitive to weak fundamentals. Many emerging countries despite the weaker US dollar in the recent past continue to show weak currencies, including Brazil, Russia, South Africa, and India.

This underscores the need for fiscal spending to be appropriately paced, growth-targeted and inclusive. Investing in health remains a priority. As governments prepare their budgets for 2021, fiscal expenditures to improve access to the vaccine worldwide are a first order priority. Global cooperation in fighting the pandemic has been weak so far. However, there is a sense of urgency for governments to work together and guarantee a more equitable access to the vaccine. At the same time,governments in cooperation with the private sector will do well in enforcing some positive trends that have accelerated since the crisis. Investing for the future to slowly reduce the dependence in low-carbon technologies for many oil-exporting countries, in education and digital systems are some examples.

There is no doubt that the economic impact of the COVID-19 pandemic will become more visible in the coming months when measures are withdrawn, but it will also make clearer how governments and investors are contributing to building a more sustainable future.